How to Avoid Appraisal Gaps in BRRRR Deals

Learn expert strategies to avoid appraisal gaps in BRRRR deals. Maximize your cash-out proceeds and protect your investment with accurate ARV.

How to Avoid Appraisal Gaps in BRRRR Deals

TL;DR:

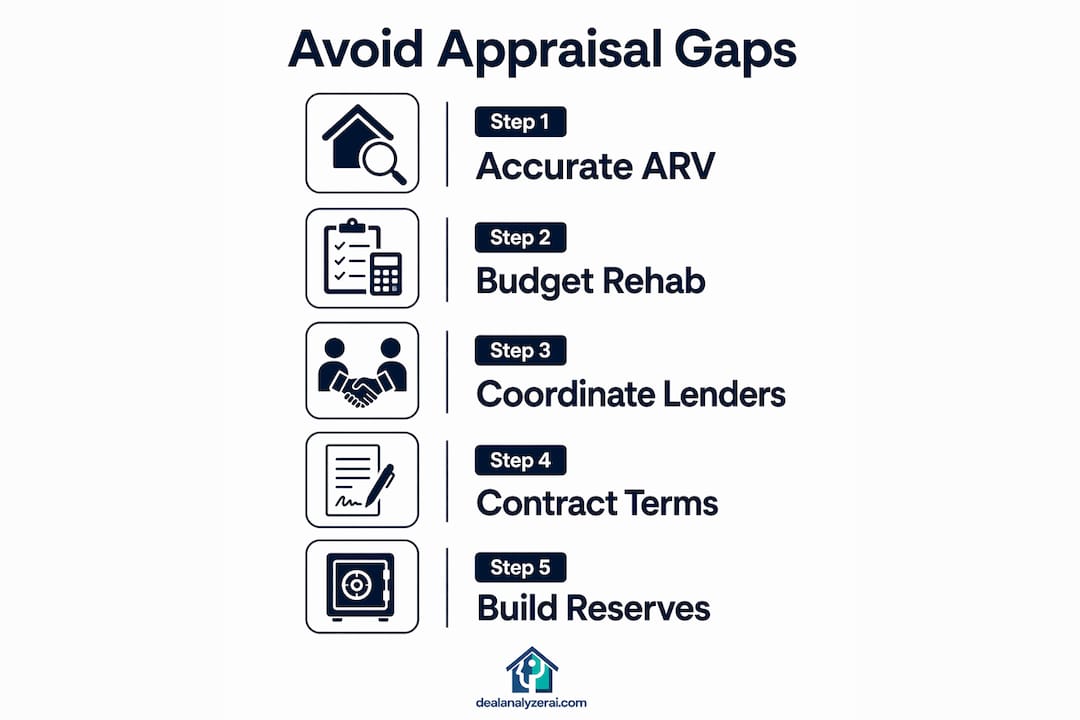

- An appraisal gap in a BRRRR deal is the difference between projected and actual appraised value at refinance, which can reduce cash-out proceeds. To avoid this risk, investors should use conservative ARV estimates, accurate rehab budgeting with contingencies, early lender coordination, and hold liquid reserves of 20-30% of project costs. Building relationships with lenders and treating low appraisals as negotiations rather than disasters can also help maintain deal viability.

An appraisal gap in a BRRRR deal is defined as the difference between your projected After Repair Value and what a licensed appraiser actually assigns to the property at refinance. This gap directly cuts your cash-out proceeds and can trap capital you planned to recycle into the next deal. Appraisals for BRRRR projects often come in 5–10% below investor ARV projections, which means a single miscalculation can cost you tens of thousands in recoverable equity. The investors who consistently avoid appraisal gaps in BRRRR deals do three things well: they calculate ARV conservatively, budget rehab costs with real contingencies, and coordinate with lenders before the first nail goes in.

How to avoid appraisal gaps in BRRRR deals with accurate ARV

ARV accuracy is the single biggest lever you control before you ever make an offer. Most appraisal gaps do not happen at the appraisal. They happen weeks earlier, when an investor accepted an optimistic number without stress-testing it.

The most common mistake is relying on a wholesaler’s ARV. Wholesalers have a financial incentive to present the highest defensible number. Their comps often include properties that are slightly larger, more recently updated, or located on a better street. Underwriting with the 25th percentile of comparables rather than the average creates a real safety margin against conservative appraisals. That lower quartile number is what a cautious appraiser will likely land on.

Strong ARV analysis uses comparables that meet all of the following criteria:

- Sold within the last 90 days, not 6 months

- Located within 0.5 miles in urban markets, 1 mile in suburban markets

- Within 20% of the subject property’s square footage

- Similar bedroom and bathroom count

- Similar construction era and condition after renovation

Pull at least five comps and remove the highest and lowest outliers. The remaining cluster gives you a defensible ARV range. ARV calculation methods compared across different approaches show that bracketing comps above and below the subject property produces the most appraisal-consistent results.

Pro Tip: Run your ARV analysis twice: once with the comps you prefer, and once with only the comps a skeptical appraiser would choose. If the two numbers differ by more than 8%, your deal has appraisal gap exposure before you even close.

How should you estimate rehab costs to prevent budget overruns?

Rehab cost overruns are the second most common cause of appraisal problems. When a project runs long or over budget, holding costs climb, the property sits in a partially finished state, and the appraisal catches conditions that reduce value.

A 15–20% contingency budget beyond initial rehab estimates is the standard for experienced BRRRR investors. That buffer covers the surprises that are statistically certain to appear: a hidden plumbing issue, a subcontractor who walks off the job, or a material price increase mid-project.

Use this process for every rehab estimate:

- Get three bids from licensed contractors. Do not accept verbal estimates. Written, itemized bids only.

- Eliminate the lowest bid. Low bids often reflect scope misunderstandings or a contractor who will ask for change orders later.

- Eliminate the highest bid. Unless the high bidder offers a clearly superior scope, the premium is not justified.

- Use the middle bid as your base. Add your 15–20% contingency on top of that number.

- Build in a timeline buffer. Typical BRRRR rehabs take 2–4 months. Plan for the longer end and price your holding costs accordingly.

Deferred maintenance flagged during a refinance appraisal can delay loan funding and reduce the appraised value. Appraisers note peeling paint, broken windows, and end-of-life HVAC systems as conditions that require repair before the loan closes. Budget for these items explicitly, not as part of the contingency.

Pro Tip: Walk the property with your contractor and your refinance lender’s appraisal checklist in hand. Lenders who do DSCR loans publish their minimum property condition requirements. Rehab to that standard, not just to what looks good.

For a detailed breakdown of how to build a line-item rehab budget, the guide on estimating rehab costs professionally covers scope categories that investors most often underestimate.

How do lender coordination and timing reduce appraisal risk?

Most appraisal gaps at refinance are preventable if you treat the acquisition and refinance as one connected process rather than two separate transactions. Coordinating lenders early prevents valuation and underwriting disconnects that show up as surprises at the worst possible moment.

Key lender requirements every BRRRR investor needs to know:

- DSCR loan seasoning: DSCR lenders typically require 30–90 days of stabilization after rehab completion and tenancy. Some require 3–6 months of ownership before they will order a full ARV appraisal.

- LTV caps: DSCR refinance loans cap at 70–75% LTV. Underwriting your deal at 75% LTV rather than 80% builds a meaningful buffer against a lower-than-expected appraisal.

- Conventional lender timelines: Conventional lenders often require 6 months of ownership before they recognize full ARV at refinance.

Using the same lender for both the rehab and refinance phases reduces appraisal variability. A unified underwriting team applies consistent methodology, which means fewer surprises when the appraiser submits the report.

Pre-qualifying with your refinance lender before purchase closes is one of the highest-value steps you can take. Get written loan approval terms contingent on appraisal and rental income. That document tells you exactly what ARV and DSCR the lender needs to fund the refinance.

If the appraisal still comes in low, you have four options. You can dispute the appraisal with documented comparable sales the appraiser missed. You can request a second appraisal from a different licensed appraiser. You can accept a partial cash-out refinance and pull less equity. Or you can hold the property longer, improve DSCR, and refinance when market conditions support a higher value.

Starting tenant placement 2–3 weeks before rehab completion compresses the vacant period and supports property stabilization before the appraisal date. A leased property with documented rental income is a stronger appraisal subject than a vacant one.

What contract terms protect you from appraisal gaps at purchase?

The purchase contract is your first line of defense against appraisal gap exposure. Most investors negotiate price and terms but overlook the appraisal language entirely.

An appraisal gap clause defines how much of the difference between the appraised value and the purchase price the buyer agrees to cover out of pocket. A capped appraisal gap clause protects buyers up to a specific dollar amount and is far safer than a full waiver. A full waiver obligates you to cover the entire gap regardless of size. A cap limits your maximum exposure.

Set your cap based on your actual liquid cash position. Calculate your available cash after the down payment, closing costs, and rehab budget. Whatever remains is your maximum gap coverage. Do not set a cap higher than that number.

| Clause type | Buyer exposure | Best use case |

|---|---|---|

| Full appraisal gap waiver | Unlimited | Avoid in BRRRR deals |

| Capped appraisal gap clause | Limited to cap amount | Competitive markets with strong comps |

| No appraisal gap clause | Zero | When you have full financing flexibility |

Seller negotiation tactics that reduce appraisal risk include requesting a price reduction tied to the appraisal result, asking for seller credits at closing to offset a potential gap, and structuring an earnest money release that protects you if the appraisal falls short. Working with an experienced investment-focused agent matters here. Agents who specialize in investor transactions know how to write these protections into standard purchase agreements without killing the deal. Understanding why property surveys matter in real estate transactions also helps you catch valuation issues before they become appraisal problems.

How much working capital do you need to survive an appraisal gap?

Capital reserves are what separate investors who survive appraisal surprises from those who lose deals. Maintaining 20–30% liquid working capital above total project costs is the standard for investors who run repeatable BRRRR operations.

That reserve serves four specific purposes: covering contractor draws when a draw schedule runs ahead of work completion, absorbing scope creep that exceeds the contingency budget, paying extended holding costs when the refinance takes longer than planned, and covering any appraisal gap cash needed to close the refinance.

| Project cost component | Example amount | Reserve target (25%) |

|---|---|---|

| Purchase price | $120,000 | Included in base |

| Rehab budget | $40,000 | Included in base |

| Holding costs (4 months) | $8,000 | Included in base |

| Total project cost | $168,000 | $42,000 |

The $42,000 reserve in this example sits in liquid accounts, not tied up in the deal. It does not earn a return. That is the cost of running a BRRRR strategy safely. Investors who treat reserves as optional find out what they are for the first time they face a $15,000 appraisal gap with no cash to bridge it.

Conservative cash flow planning also supports repeatable investing. Successful investors prioritize the refinance exit strategy early by selecting high-quality comparables and confirming DSCR thresholds before they make an offer. The reserve calculation is part of that early planning, not an afterthought.

Key Takeaways

Avoiding appraisal gaps in BRRRR deals requires conservative ARV underwriting, realistic rehab budgeting, early lender coordination, and liquid reserves equal to 20–30% of total project costs.

| Point | Details |

|---|---|

| Use lower quartile ARV | Underwrite with the 25th percentile of comps to build a buffer against conservative appraisals. |

| Budget a 15–20% rehab contingency | Add this buffer above the middle contractor bid to absorb scope creep and timeline overruns. |

| Pre-qualify with refinance lenders early | Get written approval terms before purchase closes to confirm ARV and DSCR requirements. |

| Cap appraisal gap clauses at your liquid limit | Never waive the full gap; set the cap at what you can actually cover after all deal costs. |

| Hold 20–30% reserves above project costs | Liquid reserves cover contractor draws, holding cost overruns, and appraisal gap cash needs. |

What I’ve learned about appraisal gaps the hard way

The most expensive lesson I see investors repeat is underwriting to the ARV they want rather than the ARV an appraiser will defend. Optimism is not a strategy. A deal that only works at the top comp is a deal that does not work.

The investors I respect most treat every BRRRR deal as if the appraisal will come in 7% below their projection. They build that assumption into the offer price, the rehab budget, and the reserve calculation. If the appraisal beats that assumption, they get a pleasant surprise. If it does not, they are already covered.

Building relationships with two or three lenders who specialize in BRRRR and DSCR financing changes everything. Those lenders tell you upfront what they need to see at refinance. They share their appraisal checklists. They flag deals that will not work before you waste six months finding out. That relationship is worth more than any single deal.

The other shift that matters is treating a low appraisal as a data point, not a disaster. A low appraisal does not have to kill a BRRRR deal. It requires a strategic adjustment: dispute it, accept a smaller cash-out, or hold longer. Investors who panic at a low appraisal have not built the reserves or the mindset to run this strategy at scale. The ones who thrive treat it as a negotiation, not a verdict.

— Sam

Dealanalyzerai tools that help you build appraisal-proof BRRRR deals

Knowing the right strategies is one thing. Running the numbers fast enough to act on them is another.

Dealanalyzerai gives BRRRR investors an AI-powered deal analysis tool that calculates ARV ranges, maximum allowable offers, and rehab cost estimates from comparable sales and uploaded property photos. The free ARV calculator pulls recent comps and flags the lower quartile value so you underwrite conservatively from the start. The rehab cost estimator generates line-item budgets that include contingency ranges, giving you a number you can take to a lender conversation with confidence. Investors who screen multiple properties weekly use Dealanalyzerai to cut analysis time and catch appraisal risk before it becomes a problem.

FAQ

What causes appraisal gaps in BRRRR deals?

Appraisal gaps occur when an investor’s projected ARV exceeds what a licensed appraiser assigns at refinance, typically due to overoptimistic comps, incomplete rehab, or deferred maintenance. Appraisals often come in 5–10% below investor projections on BRRRR projects.

How do I calculate a conservative ARV for a BRRRR deal?

Use the 25th percentile of recent comparable sales within 0.5 miles and 90 days, not the average. Underwriting with lower quartile comps creates a safety margin that accounts for conservative appraisal methodology.

What LTV should I underwrite for a BRRRR refinance?

Underwrite at 70–75% LTV for DSCR refinances. DSCR loans cap refinance LTV at 70–75%, and using the lower end of that range protects your cash-out if the appraisal comes in below your projection.

What is an appraisal gap clause in a purchase contract?

An appraisal gap clause defines how much of the difference between the appraised value and the purchase price the buyer agrees to cover. A capped clause limits buyer exposure to a specific dollar amount, which is safer than a full waiver in BRRRR acquisitions.

How much cash reserve do I need for a BRRRR deal?

Hold 20–30% of total project costs in liquid reserves above your initial investment. That buffer covers contractor draws, scope creep, extended holding costs, and any appraisal gap cash needed at refinance.

Recommended

Analyze Your Next Deal with AI

Get an instant ARV estimate, rehab cost analysis, and deal score — free for 7 days.

Get Free Deal Breakdown