How ARV Calculation Works in the BRRRR Strategy

Discover how ARV calculation works in the BRRRR strategy to maximize profits. Learn the key factors that influence your investment success!

How ARV Calculation Works in the BRRRR Strategy

After Repair Value (ARV) is the estimated market price of a property after renovations are complete, calculated by analyzing recent comparable sales and adjusting for property differences. In the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat), ARV is the single number that determines whether a deal works or fails. Get it right and you recycle capital efficiently. Get it wrong and you leave money locked in a property with no exit. Understanding how ARV calculation works in BRRRR is not optional for serious investors. It is the foundation of every underwriting decision, from your maximum purchase offer to your refinance expectations.

How ARV calculation works in the BRRRR strategy

ARV is not the listing price, the tax-assessed value, or a Zestimate from Zillow. It is a market-validated estimate derived from what similar, recently sold properties actually fetched in the same area after comparable renovations. That distinction matters enormously. Asking prices reflect seller aspirations, while closed sales reflect what buyers actually paid. Using the wrong data source is one of the most common and costly mistakes investors make.

In the BRRRR model, ARV drives three critical decisions. First, it sets your maximum allowable offer (MAO) on the purchase. Second, it defines the ceiling on your rehab budget. Third, it determines how much a lender will loan you in the refinance step, since most lenders cap cash-out refinances at 75% loan-to-value (LTV) based on the appraised post-renovation value. If your ARV estimate is inflated, all three numbers go wrong simultaneously.

The risks compound quickly. An ARV overestimation of 10% can cause investors to leave over 30% of their capital locked in a deal, which directly undermines the capital-recycling core of the BRRRR strategy. That is not a rounding error. That is a deal that fails to scale.

- ARV is based on closed sales data, not active listings or automated estimates

- Lenders use certified appraisers whose valuations may differ from your investor estimate

- ARV sets the ceiling for both your purchase price and your refinance loan amount

- A wrong ARV cascades into every other number in your deal model

Pro Tip: Treat your investor ARV estimate as a starting point, not a final answer. Lender appraisers apply strict rules around comp proximity, sale recency, and finish quality. Your number and their number can diverge significantly, so always stress-test your deal at 5% to 10% below your ARV estimate.

How to accurately calculate ARV for a BRRRR property

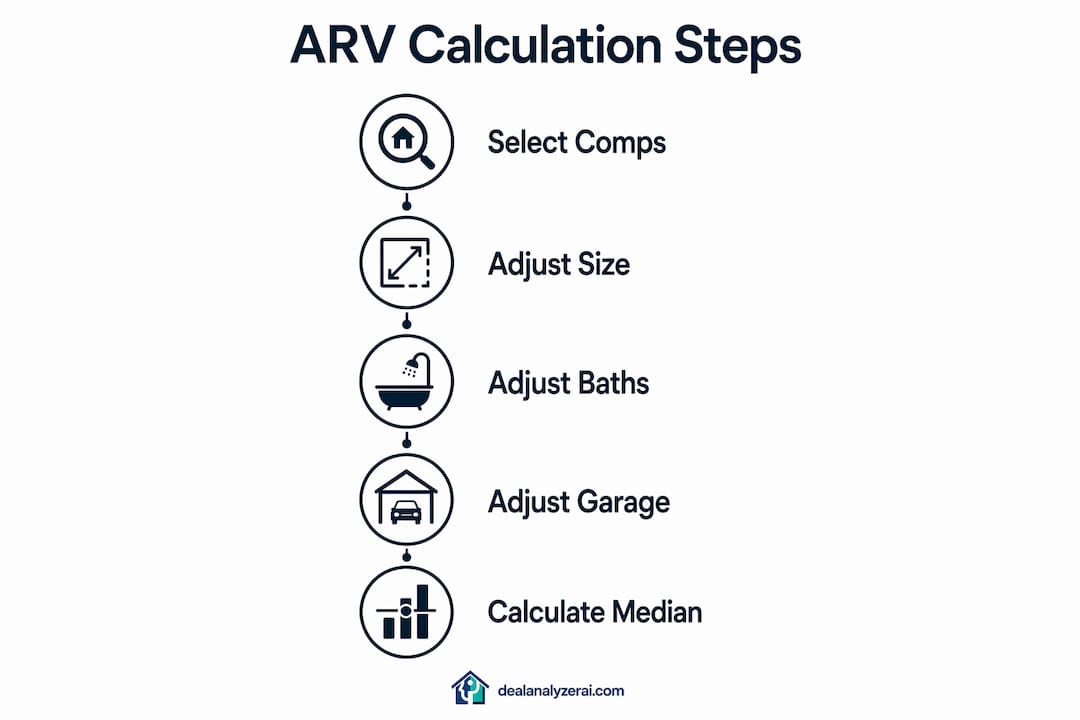

The ARV calculation process follows a structured methodology that mirrors what a licensed appraiser does, though investors apply it faster and with less formality. Here is the step-by-step process used by experienced BRRRR investors in 2026.

-

Pull 3 to 5 comparable sold properties. Use closed sales within the last 6 months and within 0.5 to 1 mile of your subject property. The industry-standard ARV calculation requires this proximity and recency to produce a defensible number.

-

Match property characteristics. Comps should share similar square footage, bedroom and bathroom count, lot size, age, and construction type. A 1,200-square-foot ranch does not comp against a 2,000-square-foot two-story, even on the same street.

-

Make line-item adjustments. Every difference between a comp and your subject property gets a dollar adjustment. Standard adjustment ranges include $8,000 to $15,000 per extra bedroom, $5,000 to $12,000 per extra bathroom, $10,000 to $20,000 for a garage, and $30 to $60 per square foot for size differences.

-

Calculate the adjusted value for each comp. If a comp sold for $310,000 but has one extra bathroom your subject property lacks, subtract $8,000 to get an adjusted value of $302,000.

-

Use the median adjusted value as your ARV. Median adjusted comps reduce distortion from atypical sales far better than a simple average. If your five adjusted comp values are $295,000, $302,000, $308,000, $315,000, and $340,000, the median is $308,000, not the $312,000 average skewed by the outlier.

Here is a simplified example of the adjustment table in practice:

| Comp | Sale Price | Size Adj. | Bath Adj. | Garage Adj. | Adjusted Value |

|---|---|---|---|---|---|

| Comp A | $305,000 | +$6,000 | $0 | $0 | $311,000 |

| Comp B | $318,000 | $0 | -$8,000 | $0 | $310,000 |

| Comp C | $295,000 | +$9,000 | $0 | +$15,000 | $319,000 |

| Comp D | $322,000 | -$6,000 | $0 | $0 | $316,000 |

| Comp E | $300,000 | +$6,000 | +$5,000 | $0 | $311,000 |

The median adjusted value here is $311,000. That becomes your working ARV.

Pro Tip: Pull your comps from the MLS or county records, not from consumer-facing platforms. MLS data includes days on market, price reductions, and seller concessions that consumer platforms strip out. Those details change your read on what a comp actually proves.

You can also cross-check your manual work against an AI-powered ARV calculator to catch adjustment errors before you make an offer.

Common pitfalls in ARV estimation for BRRRR investors

Most ARV errors are not math errors. They are judgment errors made before the calculator ever opens. Knowing where investors consistently go wrong is as valuable as knowing the formula.

The most frequent mistake is using active listing prices as proxies for market value. Only closed comps sold within 6 months should anchor your ARV. A neighbor listing at $350,000 tells you nothing about what buyers will actually pay.

Finish quality is another area where investors routinely miscalculate. Appraisers match finish quality between comps and the subject property. If your rehab produces granite countertops and luxury vinyl plank flooring in a neighborhood where comps have laminate and carpet, the appraiser will not give you full credit for the upgrade. The market sets the ceiling, not your renovation invoice.

“ARV should be viewed as a range, with conservative underwriting at the lower bound to account for appraisal discrepancies and market fluctuations.” — OffMarket Deck

The 2026 interest rate environment adds another layer of complexity. With mortgage rates above 7%, refinance caps tighten and cash flow margins compress. A deal that penciled at 4% rates in 2021 may not work today even with an identical ARV. Your ARV calculation must account for what the refinance actually costs at current rates, not historical ones.

Padding your renovation budget by 10% to 25% is not pessimism. It is discipline. Scope creep, permit delays, and material costs all push rehab numbers higher. If your ARV-based budget has no margin, one contractor surprise kills the deal.

How ARV guides your BRRRR budget and investment decisions

ARV is the anchor for every financial decision in a BRRRR deal. The most widely used formula is the 70% rule: Maximum Allowable Offer equals ARV multiplied by 70%, minus estimated rehab costs. Using the 70% rule formula with an ARV of $332,000 and $50,000 in rehab costs, the maximum offer is $182,400. That margin covers profit, closing costs, and financing expenses.

The refinance step is where ARV directly converts into cash. Most lenders cap cash-out refinances at 75% LTV based on the appraised value. Successful BRRRR investors keep total costs (purchase, rehab, closing, and holding) at or below 70% to 75% of ARV to ensure the refinance loan covers most of their invested capital. Recycling 80% or more of your initial investment is a strong outcome. Recycling 100% means the deal effectively cost you nothing outside of capital.

Here is how ARV affects deal viability across different scenarios:

| Scenario | ARV | Total Cost | LTV at Refi (75%) | Capital Recycled |

|---|---|---|---|---|

| Strong deal | $300,000 | $210,000 | $225,000 | 100%+ |

| Acceptable deal | $300,000 | $225,000 | $225,000 | 100% |

| Marginal deal | $300,000 | $240,000 | $225,000 | 94% |

| Weak deal | $300,000 | $260,000 | $225,000 | 87% |

The difference between a strong deal and a weak deal is often not the purchase price. It is an ARV estimate that was 8% too high. That is why ARV calculation methods deserve serious attention before you make any offer.

Pro Tip: Run your BRRRR numbers with a dedicated BRRRR deal calculator that models the full cycle, including refinance proceeds, rental income, and remaining equity. Spreadsheets miss interdependencies that purpose-built tools catch automatically.

Why I think most investors underestimate ARV complexity

Most investors treat ARV as a lookup task. Pull some comps, average the prices, and move on. That approach works until it doesn’t, and when it fails, it fails expensively.

The part that took me the longest to internalize is that your ARV and the appraiser’s ARV are two different numbers until proven otherwise. I have seen deals where an investor’s ARV was $330,000 and the appraisal came in at $295,000. The investor had used comps from a slightly better street, ignored a condition adjustment, and selected an outlier sale. The deal still closed, but the investor left $26,000 in equity they could not pull out.

The fix is not more comps. It is better comps with honest adjustments. Investors who consistently nail ARV are the ones who have spent time learning how appraisers think, not just how to run numbers. They know which features appraisers credit and which they discount. They know that a renovated kitchen in a C-class neighborhood adds less value than the same kitchen in a B-class neighborhood.

My strongest recommendation for volatile markets is to build your deal model around a conservative ARV range rather than a single number. Planning ARV as a range with the low end as your underwriting anchor gives you flexibility when the appraisal comes in below expectations. If the deal still works at the low end, you have a real deal. If it only works at the high end, you have a hope.

Technology helps, but it does not replace judgment. AI tools like Dealanalyzerai can surface comps faster and flag adjustment errors, but the investor still has to decide which comps are truly comparable. Use the tools to speed up the process and reduce mechanical errors. Use your market knowledge to make the final call.

— Sam

Get your ARV right the first time with Dealanalyzerai

Accurate ARV calculation is the difference between a profitable BRRRR deal and capital tied up in a property that will not refinance as planned.

Dealanalyzerai gives active investors an AI-powered edge on every deal. The free ARV calculator evaluates comparable sales and delivers ARV ranges with adjustment transparency, so you see exactly how the number was built. The rehab cost estimator analyzes uploaded property photos to produce precise renovation budgets. And the full deal analysis suite models your maximum allowable offer, refinance proceeds, and risk flags in one place. Investors using Dealanalyzerai report faster screening and fewer costly surprises at the appraisal stage. Try it free before your next offer.

FAQ

What is ARV in real estate?

ARV (After Repair Value) is the estimated market value of a property after planned renovations are complete, calculated using adjusted comparable sales. It is the foundational number for underwriting BRRRR deals, flips, and renovation loans.

How do I calculate ARV for a BRRRR property?

Select 3 to 5 comparable properties sold within 6 months and 0.5 to 1 mile of your subject property, adjust each comp for differences in size, bathrooms, garages, and condition, then use the median adjusted value as your ARV.

What is the 70% rule in BRRRR investing?

The 70% rule states that your maximum allowable offer equals ARV multiplied by 70%, minus estimated rehab costs. This margin covers profit, closing costs, and financing expenses while keeping total costs within refinance limits.

Why does ARV matter for the refinance step?

Most lenders cap cash-out refinances at 75% LTV based on the appraised post-renovation value. If your ARV estimate is too high, the refinance loan will not cover your invested capital, leaving equity locked in the property.

What are the best ARV calculation tools for BRRRR investors?

Dealanalyzerai offers a free AI-powered ARV calculator that evaluates comps and delivers adjustment-transparent ARV ranges. Manual comp analysis using MLS data remains the most accurate method when paired with honest line-item adjustments.

Key takeaways

Accurate ARV calculation in BRRRR requires median-adjusted closed comps, honest line-item property adjustments, and conservative underwriting at the low end of the ARV range to protect refinance outcomes.

| Point | Details |

|---|---|

| Use closed comps only | Active listing prices inflate ARV; only sales closed within 6 months are valid. |

| Adjust every difference | Apply $8k to $15k per bedroom, $5k to $12k per bathroom, and $30 to $60 per square foot for size gaps. |

| Use median, not average | Median adjusted comp values reduce distortion from outlier sales and improve ARV reliability. |

| Apply the 70% rule | Keep total costs at or below 70% to 75% of ARV to enable a full cash-out refinance. |

| Underwrite conservatively | Build your deal model at the low end of your ARV range to survive appraisal discrepancies. |

Recommended

Analyze Your Next Deal with AI

Get an instant ARV estimate, rehab cost analysis, and deal score — free for 7 days.

Get Free Deal Breakdown