BRRRR Deal Metrics Explained for Investors in 2026

Learn what are BRRRR deal metrics and how they impact your investment success in 2026. Master these key figures to maximize returns!

BRRRR Deal Metrics Explained for Investors in 2026

TL;DR:

- BRRRR deal metrics assess whether a property investment can generate returns, recover capital, and satisfy refinancing standards.

- In 2026, lenders require a maximum all-in cost of 70% of ARV and a minimum DSCR of 1.25 for deal viability.

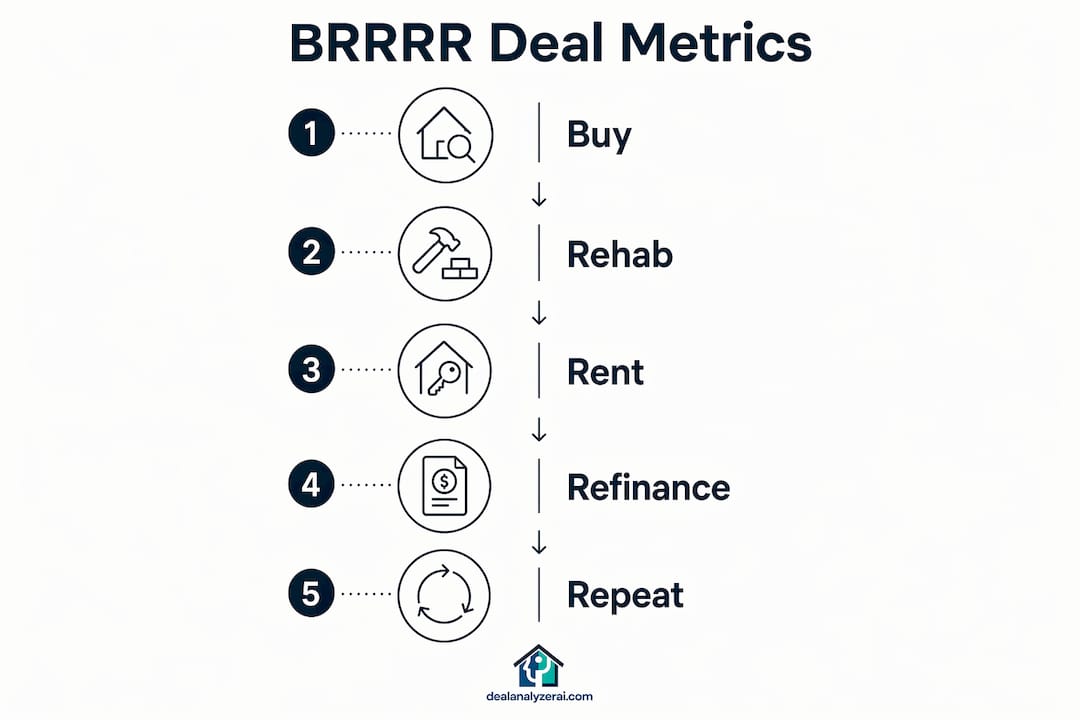

BRRRR deal metrics are quantifiable financial measures that determine whether a Buy, Rehab, Rent, Refinance, Repeat investment will generate returns, recover capital, and qualify for refinancing. The core metrics include After Repair Value (ARV), Maximum Allowable Offer (MAO), Debt Service Coverage Ratio (DSCR), cash-on-cash return, cap rate, and cash left in deal. Investors who skip these measures routinely overpay, under-rehab, or get denied at refinance. The 70% rule and a minimum DSCR of 1.25 are the two lender standards that now define deal viability in 2026. Mastering these numbers is not optional. It is the difference between a deal that builds wealth and one that ties up your capital indefinitely.

What are BRRRR deal metrics and how are they calculated?

BRRRR investment metrics are the financial inputs and outputs that measure every phase of the strategy, from acquisition through refinance. Each metric answers a specific question about deal quality, and together they form a complete picture of risk and return.

After Repair Value (ARV)

ARV is the estimated market value of a property after all renovations are complete. It drives every downstream calculation in the BRRRR model. Lenders use ARV to set the maximum loan amount at refinance, so an inflated ARV creates a false sense of security. You can learn how ARV is calculated using comparable sales within a half-mile radius, similar square footage, and recent sale dates within 90 days.

Maximum Allowable Offer (MAO)

MAO is the highest price you can pay for a property and still hit your return targets. The standard formula is: MAO = (ARV × 70%) minus rehab costs. If ARV is $200,000 and rehab costs are $30,000, your MAO is $110,000. Paying above MAO compresses your equity cushion and puts refinance proceeds at risk.

DSCR, cash-on-cash return, and cap rate

The DSCR measures whether rental income covers your mortgage payment. The formula is: DSCR = Net Operating Income / Total Debt Service. Lenders now require a minimum DSCR of 1.25 in 2026, meaning your rental income must exceed your mortgage payment by at least 25%. A DSCR below 1.25 disqualifies most cash-out refinance applications.

Cash-on-cash return measures annual pre-tax cash flow divided by total cash invested. A deal returning $6,000 per year on $50,000 invested produces a 12% cash-on-cash return. Cap rates of 6–8% reflect solid rental returns across most 2026 markets, while yields above 8% signal strong income relative to property value.

Cash left in deal

Cash left in deal equals total cash invested minus cash recovered at refinance. Zero or negative cash left means you recovered all your capital, which produces an infinite cash-on-cash return. That is the BRRRR “holy grail.” Reaching it requires accurate ARV, controlled rehab costs, and a refinance loan that covers your full investment.

Pro Tip: Run your MAO calculation using a conservative ARV, not your best-case estimate. A 5% ARV reduction on a $200,000 property cuts $10,000 from your refinance proceeds and can flip a profitable deal into a capital trap.

How have BRRRR lender standards shifted in 2026?

Lender requirements tightened significantly entering 2026, and investors who still use 2023 or 2024 assumptions are structuring deals that will fail at refinance. Three changes matter most.

The maximum all-in cost rule shifted from 75% to 70% of ARV. Higher interest rates forced lenders to demand larger equity buffers before approving cash-out refinances. A deal that cleared the 75% threshold two years ago may no longer qualify today.

The minimum DSCR rose from 1.20 to 1.25. That 0.05 difference sounds small, but on a $1,500 monthly mortgage payment it means your net operating income must now be at least $1,875 per month, not $1,800. Many markets where rents grew slowly cannot clear this bar without careful property selection.

Seasoning requirements mandate 6–12 months of ownership before most conventional lenders will base a refinance on the new appraised value rather than the purchase price. That timeline locks up your capital during rehab and the lease-up period. Planning for it upfront prevents the cash flow shock that catches unprepared investors.

Pro Tip: Build a 12-month holding cost budget into every deal before you make an offer. Include mortgage payments, insurance, taxes, and utilities for the full seasoning window. Deals that look profitable on a 3-month timeline often break even or lose money when you account for the full holding period.

How to account for rental income and expenses in BRRRR analysis

Accurate income modeling is where most BRRRR analyses fall apart. Gross rent is not the number that matters. What matters is the net income that reaches your DSCR calculation after every expense is deducted.

Realistic rental income modeling requires four adjustments before you calculate DSCR:

- Vacancy allowance. Assume 5–10% vacancy on long-term rentals. A $1,500 per month property with 8% vacancy produces $1,380 in effective gross income, not $1,500.

- Property management fees. Professional management typically costs 8–12% of collected rent. Whether you self-manage or hire out, understanding the cost of management affects your net income and DSCR directly.

- Operating expenses. Include property taxes, insurance, HOA fees, and a maintenance reserve. A common reserve is 5–10% of gross rent annually.

- Debt service. Use PITIA (principal, interest, taxes, insurance, and association dues) as your denominator in the DSCR formula, not just principal and interest.

Short-term rentals (STRs) add another layer. Lenders apply an 80% haircut to gross STR income when calculating DSCR. A property earning $3,000 per month on Airbnb is treated as $2,400 for underwriting purposes. Investors who ignore this haircut build DSCR projections that look strong on paper but collapse at the lender’s desk. For a deeper look at how rental type affects your returns, the comparison of short-term vs long-term rentals breaks down the income tradeoffs clearly.

What common pitfalls hurt BRRRR deal metric accuracy?

The most expensive mistakes in BRRRR investing are not market-driven. They are calculation errors that compound through every phase of the deal.

Overestimating ARV is the most common and most damaging error. Investors cherry-pick the highest comparable sales and ignore condition, location, or lot differences. An ARV that is 10% too high on a $200,000 property overstates refinance proceeds by $14,000 at a 70% loan-to-value ratio. That gap comes directly out of your capital recovery.

Underestimating rehab costs is the second major pitfall. Structural issues, permit delays, and material price changes routinely push budgets 15–20% over initial estimates. Always build a contingency of at least 10–15% into your rehab budget before calculating MAO.

Loan interest structure matters more than most investors realize. Dutch hard money loans charge interest on the full loan amount from day one, while Non-Dutch loans charge only on disbursed funds. On a $150,000 rehab loan drawn over six months, the difference in interest costs can reach several thousand dollars, directly increasing your all-in cost and reducing cash recovered at refinance.

Stress testing a BRRRR deal against a 5–10% ARV decline or a 10–15% rehab cost increase reveals whether your equity buffer survives adverse conditions. Deals that only work under best-case assumptions are not deals. They are bets.

Refinance seasoning delays catch investors who plan to recycle capital quickly. If your lender requires 12 months of seasoning, your capital is locked for a full year. That timeline must appear in your cash flow model from day one, not as an afterthought when the lender declines your early refinance application. Reviewing why BRRRR deals fail at refinance gives you a concrete checklist to avoid the most common disqualifiers.

Key Takeaways

Accurate BRRRR deal metrics require conservative ARV estimates, realistic expense modeling, and full compliance with 2026 lender standards including a 70% all-in cost cap and a minimum DSCR of 1.25.

| Point | Details |

|---|---|

| 70% all-in cost rule | Total acquisition and rehab costs must stay at or below 70% of ARV to qualify for refinance in 2026. |

| DSCR minimum of 1.25 | Net operating income must exceed total debt service by 25% to meet current lender underwriting standards. |

| STR income haircut | Lenders reduce short-term rental gross income by 20% before calculating DSCR, so model $2,400 for every $3,000 earned. |

| Seasoning window planning | Budget for 6–12 months of holding costs before refinance proceeds become available, or risk capital lockup. |

| Cash left in deal | Zero or negative cash left in deal signals full capital recovery and the ability to redeploy funds into the next property. |

Why I trust the numbers more than the narrative

Real estate investing attracts a lot of optimism. Sellers pitch upside. Wholesalers pitch speed. Lenders pitch flexibility. After working through dozens of BRRRR deals, the one thing that consistently separates profitable outcomes from expensive lessons is how conservatively you set your inputs before you ever make an offer.

I have seen investors run the same deal twice: once with the ARV they hoped for and once with the ARV the comps actually supported. The difference was $25,000 in projected refinance proceeds. That gap does not show up as a line item on a spreadsheet. It shows up six months later when the lender’s appraisal comes in low and the investor has to bring cash to closing instead of pulling it out.

The 2026 lender standard changes are not obstacles. They are filters that protect you from deals that would have hurt you anyway. A DSCR of 1.25 and a 70% all-in cost cap force discipline at the acquisition stage, which is exactly where discipline matters most. Investors who adapt their models to these thresholds now will structure deals that actually close and actually cash flow.

The best tool I have found for running these scenarios quickly is Dealanalyzerai. It calculates ARV ranges, flags deals that miss the 70% threshold, and models both long-term and short-term rental income with the correct lender haircuts applied. For investors screening multiple properties per week, that speed and accuracy is not a convenience. It is a competitive edge.

— Sam

Dealanalyzerai’s free BRRRR calculator puts the metrics to work

Knowing the formulas is the first step. Running them accurately on every deal you screen is where most investors lose time and make errors.

Dealanalyzerai’s free BRRRR deal analyzer calculates ARV, MAO, DSCR, cash-on-cash return, and cash left in deal using 2026 lender thresholds built directly into the model. It applies the 70% all-in cost cap, the 1.25 DSCR minimum, and the 80% STR income haircut automatically. You upload property photos and the AI estimates rehab costs from the images, removing the guesswork from your budget. Investors who use Dealanalyzerai report catching deal-killing issues before making offers, which saves both capital and time. You can also use the free ARV calculator to validate comparable sales before committing to a purchase price.

FAQ

What is the 70% rule in BRRRR investing?

The 70% rule states that your total all-in cost (purchase price plus rehab) must not exceed 70% of the property’s ARV. This threshold preserves enough equity to qualify for a cash-out refinance and recover your invested capital.

How do you calculate DSCR for a BRRRR deal?

DSCR equals Net Operating Income divided by total debt service (PITIA). A result of 1.25 or higher meets the 2026 minimum lender requirement for most cash-out refinance programs.

What does “cash left in deal” mean?

Cash left in deal is the amount of your own money still tied up in the property after refinance proceeds are received. Zero or negative means you recovered all invested capital and can redeploy it into the next deal.

How does the STR income haircut affect BRRRR metrics?

Lenders reduce gross short-term rental income by 20% before calculating DSCR, so a property earning $3,000 per month is underwritten at $2,400. Ignoring this haircut produces an overstated DSCR and a likely refinance denial.

What is a good cap rate for a BRRRR rental property?

Cap rates of 6–8% reflect solid returns across most 2026 markets. Rates above 8% indicate strong income relative to property value, while rates below 6% are common in high-appreciation metros where investors accept lower current income for long-term equity growth.

Recommended

Analyze Your Next Deal with AI

Get an instant ARV estimate, rehab cost analysis, and deal score — free for 7 days.

Get Free Deal Breakdown