How to Estimate Rental Income Before Purchase

Learn how to estimate rental income before purchase to avoid costly mistakes. Calculate effective income and ensure profitable investments.

How to Estimate Rental Income Before Purchase

TL;DR:

- Estimating rental income involves calculating effective gross income and net operating income to assess property cash flow. Investors should use independent market data, stress-test assumptions, and apply key metrics like cap rate, cash-on-cash return, and DSCR to evaluate deal viability. Systematic analysis and thorough validation help avoid overestimation and ensure reliable investment decisions.

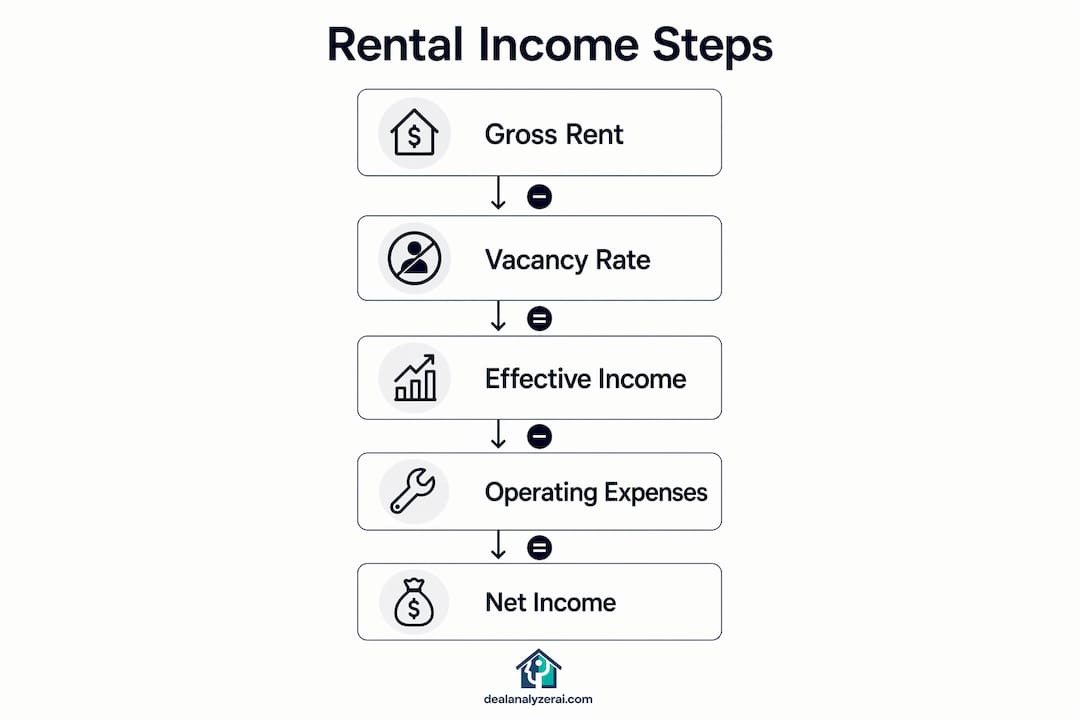

Estimating rental income before purchase is defined as calculating a property’s Effective Gross Income (EGI) and Net Operating Income (NOI) to predict cash flow before you commit to buying. Investors who skip this step routinely overpay, underestimate expenses, and watch deals turn negative within the first year. The calculation chain runs from Gross Potential Rent down through vacancy adjustments, operating costs, and debt service to arrive at actual cash flow. Metrics like NOI, cap rate, and Debt Service Coverage Ratio (DSCR) are the industry’s standard vocabulary for this process. Getting them right before closing is the difference between a performing asset and a money pit.

What data do you need to estimate rental income before purchase?

Accurate rental income estimation starts with the right inputs. Garbage data produces garbage projections, no matter how clean your spreadsheet looks.

The four data categories every investor needs are:

- Market rent comps: Pull active listings and recently leased comparables from the MLS, Zillow, and Rentometer. Use properties within a half-mile radius with similar bed/bath counts and condition. Rentometer’s percentile data shows where your target rent sits relative to the local market.

- Vacancy rates: Local property managers and county-level census data are the most reliable sources. A 5–10% vacancy assumption covers most stable markets, but tertiary markets or seasonal rentals may run higher.

- Operating expenses: Request the seller’s profit and loss statement, but treat it as a starting point, not gospel. Cross-check against the 50% rule as a sanity check (more on that below).

- Loan terms: Your lender’s rate, amortization period, and down payment requirement determine debt service, which directly affects cash flow even though it sits outside the NOI calculation.

Rental property calculators that accept all four inputs produce monthly cash flow, cap rate, and cash-on-cash return in one pass. That speed matters when you are screening multiple properties in a week.

Pro Tip: Cross-reference at least three rent comp sources before locking in your gross potential rent figure. A single Zillow listing can be an outlier that skews your entire projection.

How do you calculate EGI and NOI to predict rental returns?

The calculation chain has three steps. Each one builds on the last, and skipping any step produces a number you cannot trust.

Step 1: Gross Potential Rent

Gross Potential Rent (GPR) is the total rent the property would collect if every unit were occupied at market rate for 12 months. For a duplex with two units at $1,400 per month, GPR equals $33,600 per year.

Step 2: Effective Gross Income

EGI is calculated by multiplying GPR by one minus the vacancy rate. At a 7% vacancy assumption, EGI equals $33,600 × 0.93, which is $31,248. That figure represents realistic annual income after accounting for turnover and empty periods. Vacancy is the single most commonly understated variable in seller-provided projections.

Step 3: Net Operating Income

NOI equals EGI minus operating expenses, and mortgage payments are deliberately excluded. NOI measures the property’s performance independent of how you finance it. Operating expenses include property taxes, insurance, maintenance, property management fees, and capital expenditure reserves.

Here is a worked example for that same duplex:

| Line Item | Annual Amount |

|---|---|

| Gross Potential Rent | $33,600 |

| Vacancy (7%) | ($2,352) |

| Effective Gross Income | $31,248 |

| Operating Expenses (50%) | ($15,624) |

| Net Operating Income | $15,624 |

Operating expenses consume roughly 50–55% of gross rental income in most markets. That benchmark, known as the 50% rule, gives you a fast sanity check when a seller’s expense schedule looks suspiciously lean.

Pro Tip: Never use a seller’s stated NOI without rebuilding it from scratch using your own vacancy and expense assumptions. Sellers routinely omit capital expenditure reserves, which can run $1,500–$3,000 per unit annually.

Which financial metrics should investors use to evaluate cash flow?

NOI is the foundation, but three additional metrics tell you whether the deal actually works for your capital and your lender.

Cap rate

Cap rate equals NOI divided by the purchase price. For the duplex above with a $200,000 purchase price, cap rate equals $15,624 / $200,000, or 7.8%. Cap rate measures the property’s return independent of financing. A higher cap rate signals more income relative to price, but it can also signal higher risk or a weaker market.

Cash-on-cash return

Cash-on-cash return measures annual pre-tax cash flow divided by total cash invested. If you put $50,000 down and the property generates $6,000 in annual cash flow after debt service, your cash-on-cash return is 12%. This metric answers the question your lender’s underwriter does not: how hard is your actual cash working?

DSCR

Lenders require a DSCR of at least 1.2 to 1.25 to approve a rental property loan. DSCR equals NOI divided by annual debt service. A DSCR of 1.0 means the property barely covers its mortgage. A DSCR of 1.25 means NOI is 25% above debt payments, giving the lender a cushion. Understanding why lenders care about DSCR before you apply saves you from surprises at underwriting.

Quick cross-checks

Two fast filters help you screen deals before running full numbers:

- The 1% rule: Monthly rent should equal at least 1% of the purchase price. A $200,000 property needs $2,000 per month in rent to pass. This rule screens out obvious mismatches in seconds. Read more about using the 1% rule as a first filter before deeper analysis.

- Gross Rent Multiplier (GRM): GRM equals purchase price divided by annual gross rent. Lower GRM values indicate better relative value. Compare GRM across similar properties in the same submarket to spot outliers.

How do you stress-test rental income assumptions before committing?

A projection that only works under perfect conditions is not a projection. It is a wish. Stress-testing forces your model to answer: what happens when things go wrong?

Follow these four steps to build a resilient rental income forecast:

- Lower rent by 10–15%. Model what happens if the market softens or you cannot achieve your target rent on day one. If cash flow turns deeply negative at 85% of projected rent, the deal has no margin for error.

- Raise vacancy to 15%. A single extended vacancy in a single-family rental can push annual vacancy well above the 5–10% baseline. Test whether the deal survives a two-month vacancy per year.

- Inflate expenses by 10–20%. Insurance premiums, property taxes, and maintenance costs all rise over time. A model that ignores expense creep will underperform within three years.

- Extend your hold period analysis. Run projections at year one, year three, and year five. Rent growth and appreciation compound, but so do deferred maintenance costs and capital expenditure needs.

Stress-testing rental income by adjusting rent downward and vacancy upward is the standard method experts recommend for verifying deal viability under real market conditions.

Relying on a single valuation method risks deal failure. Layering the income approach, the 1% rule, and multi-year cash flow projections gives you a far more reliable picture of what a property will actually produce.

Seller-provided data deserves particular skepticism. Sellers have every incentive to present the most favorable income picture. Cross-referencing seller figures against independent market data and evaluating multiple properties with consistent assumptions is the only way to make fair comparisons. Relying on a seller’s pro forma rent without market validation is one of the most common mistakes in property evaluation that investors make before closing.

Key Takeaways

Accurate rental income estimation requires calculating EGI and NOI from independent market data, then stress-testing those figures against vacancy spikes, expense inflation, and rent softening before making an offer.

| Point | Details |

|---|---|

| Start with EGI | Multiply Gross Potential Rent by one minus your vacancy rate to get realistic income. |

| Build NOI from scratch | Subtract your own operating expense estimates from EGI; never rely on seller figures alone. |

| Apply three core metrics | Cap rate, cash-on-cash return, and DSCR each answer a different question about deal quality. |

| Use quick filters first | The 1% rule and GRM screen out weak deals in seconds before you run full projections. |

| Stress-test every assumption | Lower rent, raise vacancy, and inflate expenses to confirm the deal survives market shifts. |

What I’ve learned from years of running rental income projections

The single biggest mistake I see investors make is treating the income side of the equation as fixed and only questioning the expenses. Rent projections feel concrete because you can pull a Zillow comp in 30 seconds. Expenses feel abstract until a $12,000 HVAC replacement shows up in year two.

My rule: build the expense model first, then ask whether the rent supports it. That reversal changes how you read a deal. You stop asking “can I make this rent work?” and start asking “does this property generate enough income to cover what it will actually cost to own?”

The second lesson is about pro forma rents. Sellers and listing brokers routinely present “market rate” rents that reflect the top of the range, not the median. I have seen pro forma rents 18–22% above what comparable units were actually leasing for in the same zip code. Always build your own rent comp analysis using leased comparables, not active listings. Active listings are asking prices. Leased comps are reality.

Third: no single method is enough. I use the 1% rule to screen, NOI and cap rate to evaluate, and DSCR to confirm lender viability. Then I stress-test. Each method catches something the others miss. Analyzing a rental property thoroughly does not have to take days, but it does require running all the numbers, not just the ones that make the deal look good.

The investors who consistently buy well are not smarter. They are more systematic. They run the same process on every deal, they update their assumptions with fresh market data, and they walk away from deals that only pencil out under optimistic conditions.

— Sam

How Dealanalyzerai makes rental income analysis faster and more reliable

Dealanalyzerai is built for investors who need to screen multiple properties quickly without sacrificing analytical depth.

The platform’s investment property calculator runs cash flow, cap rate, NOI, and DSCR calculations simultaneously from a single set of inputs. You enter purchase price, loan terms, market rent, and expense assumptions, and the tool returns a complete income forecast in seconds. Dealanalyzerai also flags risk factors automatically, including deals where DSCR falls below lender thresholds or where the 1% rule is not met. For investors running five to ten property analyses per week, that speed and consistency is a real advantage. Visit dealanalyzerai.com to run your first analysis free.

FAQ

What is Effective Gross Income in rental property analysis?

Effective Gross Income (EGI) is Gross Potential Rent multiplied by one minus the vacancy rate. It represents the realistic annual income a property generates after accounting for vacancy and turnover.

How do I calculate Net Operating Income for a rental property?

NOI equals EGI minus all operating expenses, excluding mortgage payments. Operating expenses include taxes, insurance, maintenance, management fees, and capital expenditure reserves.

What DSCR do lenders require for rental property loans?

Most lenders require a DSCR of at least 1.25, meaning the property’s NOI must exceed annual debt service by 25%. A DSCR below 1.2 typically triggers loan denial or requires additional reserves.

What is the 1% rule and when should I use it?

The 1% rule states that monthly rent should equal at least 1% of the purchase price. Use it as a fast first filter to screen out deals before running full NOI and cash flow projections.

How do I stress-test a rental income projection?

Lower your projected rent by 10–15%, raise vacancy to 15%, and increase expense estimates by 10–20%. If the deal still produces positive cash flow under those conditions, it has a real margin of safety.

Recommended

Analyze Your Next Deal with AI

Get an instant ARV estimate, rehab cost analysis, and deal score — free for 7 days.

Get Free Deal Breakdown