How Investors Evaluate Multiple Properties Efficiently

Discover how investors evaluate multiple properties efficiently using key metrics. Optimize your real estate decisions and maximize returns!

How Investors Evaluate Multiple Properties Efficiently

Evaluating multiple investment properties simultaneously is defined as the systematic process of applying standardized financial metrics, market analysis, and portfolio-level risk assessment to rank and compare real estate opportunities before committing capital. Investors who do this well use a combination of Net Operating Income, cap rate, cash-on-cash return, and Debt Service Coverage Ratio to score each property on the same scale. Tools like Buildium, AirDNA, and Dealanalyzerai have replaced manual spreadsheets for many active investors screening five or more deals per week. The core insight is this: no single metric tells the full story. Profitable multi-property decisions require integrating financial data, local market conditions, and portfolio fit into one disciplined framework.

How investors evaluate multiple properties: the core financial metrics

The four metrics every serious investor calculates before comparing properties are NOI, cap rate, cash-on-cash return, and Gross Rent Multiplier. Each answers a different question about a property’s profitability, and together they create a complete financial picture.

Here is what each metric measures and why it matters:

- Net Operating Income (NOI): Annual rental income minus all operating expenses, excluding debt service. NOI is the foundation for every other calculation.

- Cap rate: NOI divided by purchase price, expressed as a percentage. Cap rate lets you compare yield across properties regardless of financing structure.

- Cash-on-cash return: Annual pre-tax cash flow divided by total cash invested. This metric reflects the actual return on your out-of-pocket dollars, making it the most relevant number for leveraged buyers.

- Gross Rent Multiplier (GRM): Purchase price divided by annual gross rent. A GRM below 10 is a baseline threshold for residential rental viability in most markets.

- Debt Service Coverage Ratio (DSCR): NOI divided by annual debt service. Lenders typically require a DSCR between 1.20 and 1.35, meaning the property must generate 20 to 35 percent more income than its mortgage payments. Properties with a DSCR below 1.20 often face financing challenges.

Property management fees also affect these numbers directly. Out-of-state and portfolio investors typically pay 8 to 12 percent of collected rent in management fees, which reduces NOI and, by extension, cap rate and cash flow. Ignoring this cost when screening deals is one of the most common errors newer investors make.

Pro Tip: Never rank properties using a single metric. A high cap rate can mask poor cash flow if financing costs are high. A strong cash-on-cash return can hide a weak DSCR. Run all five metrics for every property before drawing any conclusions.

How do investors analyze market and regulatory factors?

Financial metrics tell you what a property earns today. Market and regulatory analysis tells you whether that income is stable, growing, or at risk. These two layers of analysis work together in any credible property investment assessment.

The most important market factors to examine include:

- Supply and demand trends: Rising supply in a submarket compresses occupancy rates and puts downward pressure on rents. Tools like AirDNA provide supply growth rates and occupancy metrics for short-term rental markets, giving investors a forward-looking view.

- Occupancy rate trends: A property with a 90 percent occupancy rate in a market where average occupancy is falling signals a competitive advantage. A property at 75 percent in a rising market signals a management problem.

- Seasonality: Markets with extreme seasonal swings, such as beach towns or ski resorts, require investors to model monthly cash flows rather than annual averages. A property that looks profitable on an annual basis can run negative for four consecutive months.

- Local short-term rental regulations: Cities including New York, San Francisco, and Santa Monica have enacted restrictions that can eliminate short-term rental income entirely. Regulatory risk is a valuation input, not an afterthought.

Pro Tip: Research regulatory risk before running any other analysis. If a city is actively restricting short-term rentals, price that risk into your offer or walk away. Discovering a regulatory problem after closing is expensive.

What portfolio-level strategies optimize risk and returns?

Comparing individual properties in isolation misses the most important question: how does this deal change the overall portfolio? Experienced investors treat each acquisition as a portfolio decision, not just a property decision.

Concentration risk is the primary danger at the portfolio level. An investor who owns five single-family rentals in the same zip code, all rented to tenants in the same industry, faces correlated risk across every asset. A single employer layoff or local economic shock can trigger simultaneous vacancies across the entire portfolio.

Diversification across three axes reduces this exposure:

- Asset type: Mixing single-family rentals, small multifamily, and short-term rentals creates income streams that respond differently to economic cycles.

- Geography: Properties in different metro areas or states are exposed to different job markets, regulatory environments, and supply pipelines.

- Tenant mix: Residential, commercial, and vacation rental tenants behave differently during downturns, providing a natural hedge.

AI portfolio optimization models process property correlations across markets, property types, tenant industries, and debt structures to identify diversification gaps that human analysis misses. Institutional-grade analytics of this kind have been shown to improve returns by 15 to 25 percent through smarter diversification and risk management. That is a meaningful edge for investors managing more than five properties.

Portfolio stress testing considers macroeconomic shocks, tenant defaults, and regulatory changes across all properties simultaneously to evaluate aggregate risk and resilience. This is the standard that separates institutional investors from retail investors.

Practical portfolio management also requires aggregating financials across all properties in one place. Platforms like Buildium and AppFolio allow investors to track income, expenses, and occupancy at the portfolio level rather than property by property. Experienced investors also negotiate partial release clauses in blanket mortgages, which allows the sale or payoff of individual properties without triggering defaults on the entire portfolio loan. That flexibility is worth negotiating for before you need it.

How do scenario modeling and dual rental analyses improve evaluation?

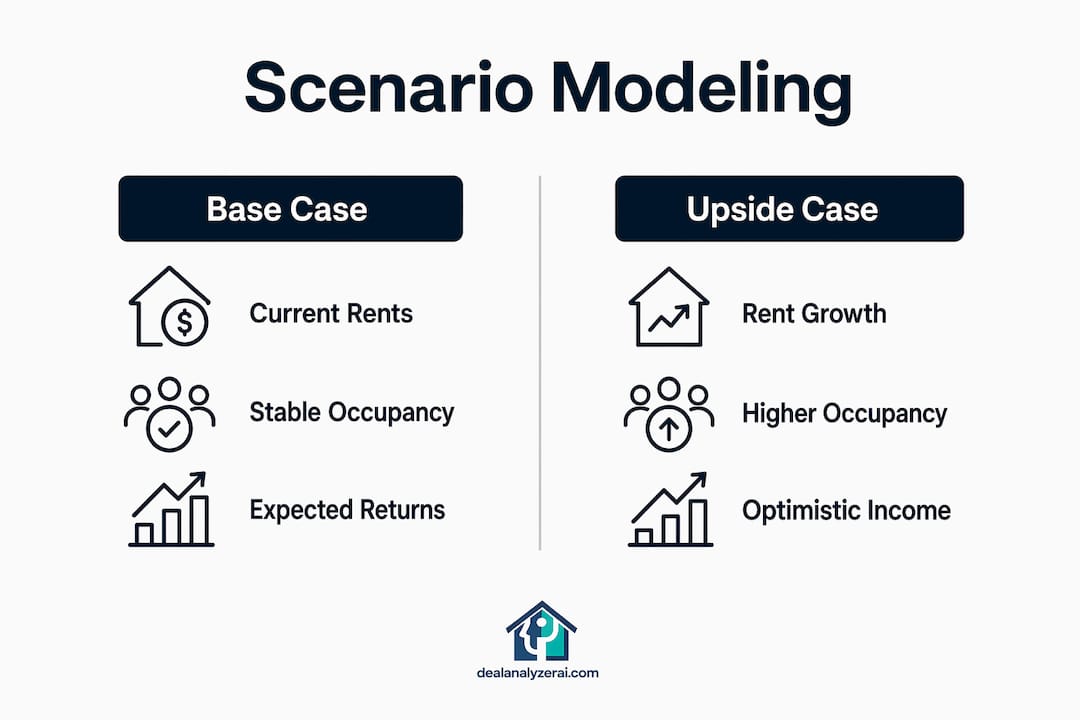

A single revenue projection is not an analysis. It is a guess. Professional investors build at least four scenarios for every property they seriously consider: base case, upside, downside, and stress test.

The base case uses current market rents and realistic occupancy. The upside case models what happens if rents grow at the market trend rate and occupancy improves. The downside case tests what happens if vacancy rises, rents soften, or a major capital expense hits in year two. The stress test pushes assumptions to their limits: vacancy spikes up to 15 percent, rent declines of 10 to 15 percent, and unexpected capital expenses layered on top of each other. The goal is not to predict the worst case. The goal is to find the break point where the investment stops being profitable.

| Scenario | Key Assumptions | Purpose |

|---|---|---|

| Base case | Current rents, stable occupancy | Establishes expected return |

| Upside | Rent growth, improved occupancy | Defines ceiling potential |

| Downside | Vacancy increase, flat rents | Tests cash flow resilience |

| Stress test | 15% vacancy, rent decline, capex hit | Identifies break-even threshold |

Dual rental analysis adds another dimension to this process. Analyzing properties as both short-term and long-term rentals gives investors a floor and a ceiling for income potential. The long-term rental income is the floor: the stable, predictable baseline the property can generate regardless of platform changes or regulatory shifts. The short-term rental income is the ceiling: the maximum revenue achievable under favorable conditions. A property that only works as a short-term rental carries concentrated risk. A property that works as both offers operational flexibility.

Pro Tip: Use at least two independent data sources for revenue estimates. AirDNA, local property managers, and direct Airbnb market data often produce different numbers. The conservative estimate is the one to build your base case around.

How to practically organize and compare multiple properties

The biggest operational challenge in multi-property investment strategies is keeping analysis consistent across deals. When every property gets evaluated differently, comparisons become meaningless.

A standardized financial model solves this problem. Build one spreadsheet template that calculates NOI, cap rate, cash-on-cash return, GRM, and DSCR automatically when you input purchase price, rents, expenses, and financing terms. Apply the same template to every property you screen. This creates an apples-to-apples comparison across any number of deals.

Software platforms take this further. Platforms like Buildium and Dealanalyzerai allow investors to systematically compare multiple properties and monitor portfolio health from a single dashboard. Dealanalyzerai specifically addresses the two most inconsistent inputs in property analysis: ARV estimates and rehab cost projections. Its AI algorithms evaluate comparable sales and analyze uploaded property photos to generate precise cost estimates, which removes the guesswork that distorts most manual analyses.

Key criteria to rank properties against each other:

- Cap rate vs. local market average: A cap rate 50 basis points above the local average signals either a bargain or a problem worth investigating.

- Cash flow after debt service: Positive cash flow is the minimum threshold. The question is how much cushion exists above break-even.

- Portfolio fit score: Does this property reduce concentration risk or increase it? Does it add geographic diversification or duplicate existing exposure?

- Regulatory risk rating: Is the local regulatory environment stable, tightening, or uncertain?

Pro Tip: Delegate day-to-day property management before you scale past three properties. Tracking performance through a dashboard is only possible when you are not also handling maintenance calls. Standard operating procedures for tenant screening, maintenance, and reporting make the data reliable.

Use the rental cash flow calculator to run consistent numbers across every property you screen, so your comparisons reflect real data rather than optimistic assumptions.

Key takeaways

Investors who evaluate multiple properties successfully combine standardized financial metrics, market analysis, portfolio-level diversification, and scenario modeling into one repeatable process.

| Point | Details |

|---|---|

| Use five core metrics | NOI, cap rate, cash-on-cash return, GRM, and DSCR must all be calculated for every property. |

| Regulatory risk is a valuation input | Research local short-term rental laws before running financial projections. |

| Diversify across three axes | Asset type, geography, and tenant mix reduce correlated risk across the portfolio. |

| Build four scenarios per property | Base, upside, downside, and stress test cases reveal break points before you close. |

| Standardize your analysis process | One spreadsheet template or platform applied consistently makes comparisons meaningful. |

What I’ve learned from watching investors get this wrong

The most common mistake I see is investors who treat each property as a standalone decision. They find a deal with a strong cap rate, run the numbers in isolation, and move forward without asking how it changes the portfolio they already own. Then they wonder why their returns are volatile. The answer is almost always concentration risk they did not see because they never looked for it.

The second pattern I notice is over-reliance on optimistic projections. Investors who build their base case on best-case occupancy and peak-season revenue are not doing analysis. They are doing wishful thinking with a spreadsheet. Conservative assumptions and stress testing are what separate investors who survive market corrections from those who do not. The break-even analysis is not a pessimistic exercise. It is the most important number in the model.

AI and data analytics have genuinely changed what is possible here. The ability to process correlations across a portfolio, flag concentration risks automatically, and generate scenario models in minutes used to require institutional resources. Now it is available to individual investors through tools like Dealanalyzerai. The investors who adopt these tools early will have a structural advantage over those still working from intuition and manual spreadsheets.

One more observation: regulatory risk is consistently underpriced. Investors who buy in markets with active short-term rental restrictions and do not account for that risk in their offer price are taking on uncompensated exposure. The dual rental analysis framework is the right way to handle this. Know what the property is worth as a long-term rental before you pay a premium for short-term rental upside.

— Sam

See how Dealanalyzerai handles multi-property analysis

Screening multiple deals every week requires a process that is fast, consistent, and accurate. Dealanalyzerai is built specifically for active investors who need ARV ranges, maximum allowable offers, rehab cost estimates, and cash flow projections in one place, without rebuilding a spreadsheet for every deal.

The platform’s AI algorithms analyze comparable sales and uploaded property photos to generate precise cost estimates, which removes the two biggest sources of error in manual deal analysis. Investors using Dealanalyzerai report catching risk flags before making offers, which translates directly into avoided losses. Try the free AI deal analyzer to run your next property through a complete financial analysis, or use the cash flow calculator to stress-test your assumptions before you commit.

FAQ

What financial metrics matter most when comparing investment properties?

The five metrics that matter most are NOI, cap rate, cash-on-cash return, GRM, and DSCR. No single metric is sufficient on its own. Running all five for every property creates a consistent basis for comparison.

What DSCR do lenders require for investment property loans?

Most lenders require a DSCR between 1.20 and 1.35, with 1.25 as the most common standard. Properties below 1.20 typically face financing challenges or require larger down payments.

How does dual rental analysis help evaluate a property?

Dual rental analysis compares a property’s income potential as both a short-term and long-term rental. The long-term rental figure sets the income floor, while the short-term rental figure defines the ceiling, giving investors a clear picture of risk and upside.

Why is portfolio-level analysis important when buying multiple properties?

Individual properties can look strong in isolation while introducing concentration risk at the portfolio level. Evaluating how each acquisition affects geographic, asset-type, and tenant-mix diversification prevents correlated losses across the portfolio.

How do scenario models improve investor decisions on properties?

Scenario models test base, upside, downside, and stress cases to identify the break point where a property stops being profitable. This process reveals risk that optimistic single-point projections always hide.

Recommended

Analyze Your Next Deal with AI

Get an instant ARV estimate, rehab cost analysis, and deal score — free for 7 days.

Get Free Deal Breakdown