How to Price Motivated Seller Properties Right

Learn how to price motivated seller properties right for profitable deals. Master pricing tactics and maximize your purchase potential today!

How to Price Motivated Seller Properties Right

TL;DR:

- Motivated seller properties require careful pricing based on genuine urgency, equity, and true market value. Rely on public records and real signals, not listing descriptions, to identify sellers with real distress, and score their negotiation potential objectively. Using data-driven offers and strategic concessions can close deals faster and more reliably than price cuts alone.

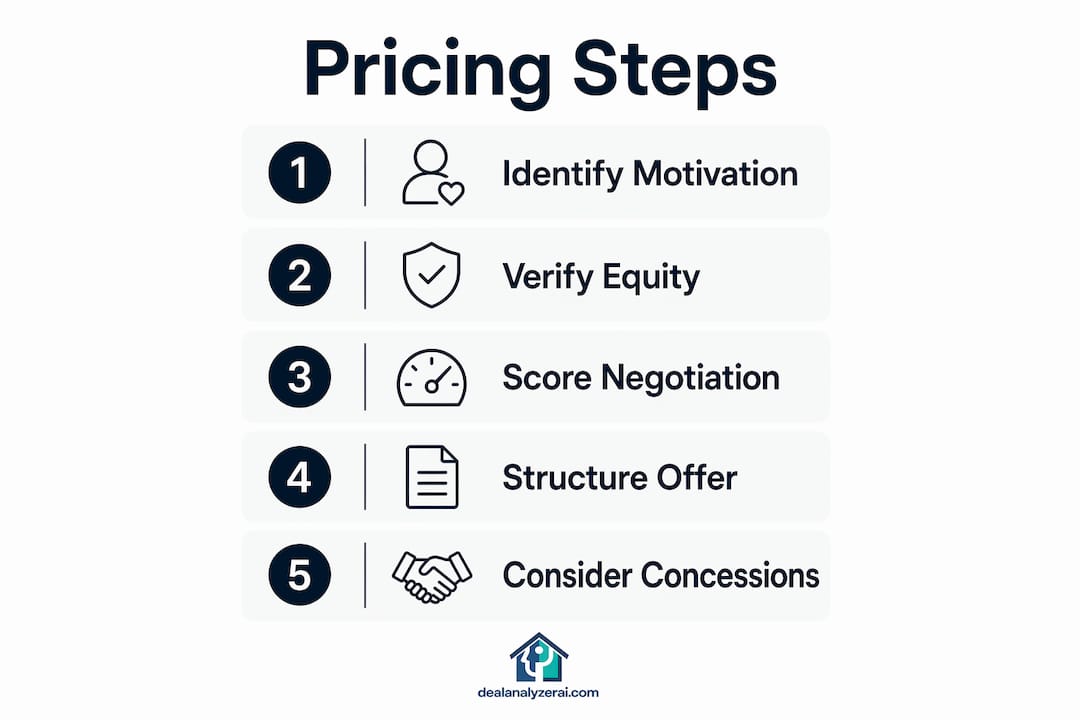

Pricing motivated seller properties right means calculating an offer that reflects the seller’s genuine urgency, their equity position, and the property’s true after-repair value. The industry term for this process is “distressed property acquisition pricing,” and it sits at the core of every profitable off-market deal. Motivated sellers, defined as owners who prioritize speed and certainty over maximum price, typically accept discounts of 10–30% below market value depending on their circumstances. Pre-foreclosure sellers often accept 25–30%, divorce or probate sellers 15–25%, and tired landlords closer to 10–15%. Getting the number right requires more than finding a cheap motivated seller property. It demands a disciplined process for reading motivation signals, scoring negotiation room, and structuring offers that solve the seller’s actual problem.

How to price motivated seller properties right: start with real motivation signals

The phrase “motivated seller” appears in thousands of MLS listings every week. Most of those listings are marketing copy, not genuine distress signals. Sellers labeled “motivated” in listings often lack real financial or personal pressure. Investors who rely on listing language alone overpay or waste time chasing leads that go nowhere.

Real motivation shows up in data, not descriptions. Public records reveal the signals that matter: tax delinquency, vacancy status, recent probate filings, divorce court records, and pre-foreclosure notices. Life events account for over 74% of off-market motivated seller transactions. That figure tells you where to focus your sourcing energy before a property ever hits the open market.

Green lights vs. red flags in seller motivation

Green lights include multiple overlapping distress signals on the same property: a vacant home with delinquent taxes owned by an out-of-state landlord who inherited the property. Red flags include a single “motivated seller” tag on a freshly listed home with no price history, no vacancy, and a seller who has never missed a payment.

The single most effective qualifying question is direct: “What happens if you don’t sell by your target date?” That question separates sellers with a genuine deadline from sellers who are simply testing the market. A seller who answers with a concrete consequence, such as foreclosure, relocation, or probate court pressure, is a real lead. A seller who shrugs has a preference, not a problem.

Pro Tip: Apply an equity filter before spending time on any lead. High equity above 40% confirms the seller can accept a below-market offer and still walk away with cash. Without that cushion, even a genuinely motivated seller cannot say yes to your number.

Evaluating negotiation potential and structuring the right offer

Once you confirm genuine motivation, the next step is scoring the negotiation room. A point-based scorecard assigns weight to each distress signal and listing behavior. Listings scoring 8 or more points on negotiation indicators signal strong price and term flexibility. Scores of 4–7 suggest moderate room. Scores below 4 mean the seller likely has a preference, not a pressing need.

Here is a practical scoring framework investors use to evaluate urgency and flexibility:

- Vacancy confirmed (2 points): An empty property carries holding costs the seller wants to stop.

- Tax delinquency on record (2 points): Unpaid taxes signal financial strain and a real deadline.

- Price reduction history (2 points): Two or more cuts in 60 days show the seller is chasing the market down.

- Life event trigger (2 points): Probate, divorce, or foreclosure filing confirms external pressure.

- Out-of-state ownership (1 point): Absentee owners prioritize convenience over price.

- Days on market over 90 (1 point): Extended time on market erodes seller confidence.

A score of 8 or above justifies an aggressive opening offer. A score of 4–7 calls for a moderate discount with creative terms. Below 4, move on or revisit after circumstances change.

Concessions often close deals faster than price cuts

Seller-paid closing costs and repair credits frequently close deals faster than headline price reductions. A seller who needs $180,000 to pay off a mortgage and cover moving costs may reject a $175,000 offer but accept $180,000 with $6,000 in closing cost credits. The net to you is the same. The net to them feels like a win. Understanding that distinction is what separates investors who close from investors who negotiate in circles.

Pro Tip: Review listing price strategy data for your target market before structuring concessions. Local pricing trends tell you how much room sellers typically expect to give, which anchors your opening offer more credibly.

A step-by-step approach to sourcing discounted real estate listings

Finding urgently selling homes at scale requires a repeatable system, not luck. The process below applies whether you are screening five properties a week or fifty.

- Build a data-stacked lead list. Pull records combining high equity (above 40%), vacancy status, tax delinquency, and ownership type. Combining these filters narrows a county-wide list down to the highest-probability leads.

- Score every lead before outreach. Use the six-point scorecard above. Only contact leads scoring 4 or higher. This protects your time and keeps your conversion rate meaningful.

- Tailor your first message to the seller’s situation. A probate heir gets a different message than a tired landlord. Reference the specific circumstance without being intrusive. Sellers respond to investors who demonstrate they understand the situation.

- Lead with speed and certainty in your offer. Cash offers with flexible closing dates outperform higher-priced contingent offers with motivated sellers. State your closing timeline in the first conversation.

- Coordinate closing logistics early. Introduce your title company or closing attorney before the seller asks. Sellers who feel the process is organized are less likely to back out or re-trade.

- Track responsiveness and refine your scoring. Log which signals predicted actual closes. Adjust your scorecard weights based on real outcomes in your market.

The properties that produce the best returns are rarely the ones with the biggest advertised discounts. They are the ones where you identified real motivation early, scored the lead accurately, and moved faster than other investors.

What to include in your outreach messaging

Effective outreach for affordable properties for sale from motivated sellers covers three things: acknowledgment of the seller’s situation, a clear statement of what you offer (speed, cash, certainty), and a single low-friction call to action. Skip the pitch. Ask one question. “Would a cash offer with a 14-day close be worth a conversation?” That structure works across direct mail, cold call, and text campaigns.

For pre-foreclosure leads specifically, the pre-foreclosure deal analysis process differs from standard acquisition. The seller’s timeline is set by the court, not by preference, which changes how you frame urgency in your offer.

Common pitfalls when pricing motivated seller homes

Most pricing mistakes with motivated seller homes fall into a small set of repeatable errors. Recognizing them before they cost you a deal is the fastest way to improve your close rate.

- Chasing label-motivated sellers. A listing that says “motivated seller” with no supporting data signals is a time sink. Rely on objective distress indicators, not listing copy.

- Assuming price alone wins the deal. Sellers under pressure often care more about certainty than cents. An offer $10,000 lower with a guaranteed close beats a higher offer with financing contingencies.

- Ignoring title issues. Probate and divorce properties frequently carry title complications. Unresolved liens or contested ownership kill deals at closing. Pull a preliminary title report before you make an offer.

- Misjudging timing shifts. A seller who was urgent in january may have stabilized by march. Motivation is not static. Re-qualify leads that have gone cold before reengaging.

- Over-negotiating on price after inspection. Inspection results give you legitimate renegotiation room, but grinding a motivated seller on every line item destroys trust and often kills the deal entirely.

“Motivated sellers are rational actors solving a problem. They are not uninformed about market value. They are choosing speed and certainty over price. Investors who approach the negotiation with respect for that choice close more deals than those who treat the discount as an entitlement.”

The negotiation process with motivated sellers works best when you treat the seller’s urgency as a shared problem to solve, not a weakness to exploit. That mindset produces repeat referrals and a reputation that generates inbound leads over time.

Key takeaways

Pricing motivated seller properties right requires stacking real distress signals, scoring negotiation room objectively, and structuring offers around speed and certainty rather than price alone.

| Point | Details |

|---|---|

| Verify real motivation | Use public records and life event triggers, not listing labels, to confirm genuine seller urgency. |

| Apply the equity filter | Leads with equity above 40% can accept below-market offers and still close with cash in hand. |

| Score before you call | An 8-point scorecard predicts negotiation room and protects your outreach time. |

| Lead with speed and certainty | Cash offers with flexible closing dates outperform higher-priced contingent offers with motivated sellers. |

| Use concessions strategically | Closing cost credits and repair credits often close deals faster than equivalent price reductions. |

What I’ve learned about pricing these deals after years in the field

The biggest mistake I see investors make is treating “motivated seller” as a category rather than a spectrum. Two sellers in foreclosure can have completely different levels of urgency depending on how far along the process is, whether they have family support, and whether they have already mentally moved on. I have walked away from deals that looked perfect on paper because the seller’s motivation was softer than the data suggested. And I have closed deals that looked marginal because the seller had a hard deadline nobody else had bothered to ask about.

The question “What happens if you don’t sell by then?” is the single most valuable tool I use. Most investors skip it because it feels blunt. It is blunt. It is also the only way to know whether you are talking to someone with a real problem or someone who would rather wait for a better offer.

I have also learned to stop obsessing over the headline discount. A 20% price cut sounds great until you realize the seller expects you to absorb $30,000 in deferred maintenance and a title dispute. The deal scoring approach I now use weights condition, title clarity, and closing certainty alongside price. That combination tells me far more than the discount percentage alone.

The investors who consistently find the best deals on homes from motivated sellers are patient, disciplined, and genuinely curious about the seller’s situation. They are not the loudest bidders. They are the most prepared.

— Sam

How Dealanalyzerai helps you price motivated seller deals with confidence

Knowing a seller is motivated is only half the equation. You still need accurate numbers on after-repair value, rehab costs, and maximum allowable offer before you can commit to a price.

Dealanalyzerai gives investors instant ARV ranges, MAO calculations, and rehab cost estimates powered by AI analysis of comparable sales and uploaded property photos. That means you can screen a motivated seller lead in minutes, not days, and arrive at your offer with data behind it rather than gut feel. Investors using Dealanalyzerai report catching deal-killing issues before making offers, which protects capital and keeps closing timelines intact. Run your next motivated seller property through the free deal analyzer and see exactly what the numbers support before you pick up the phone.

FAQ

What discount can I expect from a motivated seller?

Motivated sellers typically accept 10–30% below market value, with pre-foreclosure sellers at the higher end and tired landlords at the lower end. The actual discount depends on urgency, equity, and how many competing offers the seller receives.

How do I confirm a seller is genuinely motivated?

Ask directly what happens if they do not sell by their target date. Sellers with real urgency give concrete answers tied to financial or legal consequences. Sellers without real urgency give vague or flexible responses.

What equity level makes a motivated seller lead viable?

Equity above 40% is the standard threshold for a viable motivated seller lead. Below that level, the seller may not have enough room to accept a below-market offer and still clear their mortgage and closing costs.

Should I prioritize price cuts or concessions in my offer?

Concessions like closing cost credits and repair credits often close deals faster than equivalent price reductions. They preserve the seller’s stated price while reducing your net cost, which makes both sides feel like they won.

How do I find motivated seller properties before they hit the MLS?

Stack public record filters including vacancy, tax delinquency, probate filings, and out-of-state ownership to build a pre-market lead list. The off-market property search process consistently surfaces urgently selling homes before other investors see them.

Recommended

Analyze Your Next Deal with AI

Get an instant ARV estimate, rehab cost analysis, and deal score — free for 7 days.

Get Free Deal Breakdown